Page 39 - Bullion World Issue 01 Volume 06 January_2026

P. 39

Bullion World | Volume 6 | Issue 01 | January 2026

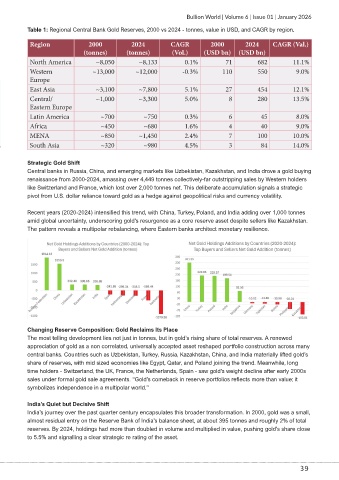

Table 1: Regional Central Bank Gold Reserves, 2000 vs 2024 - tonnes, value in USD, and CAGR by region.

Region 2000 2024 CAGR 2000 2024 CAGR (Val.)

(tonnes) (tonnes) (Vol.) (USD bn) (USD bn)

North America ~8,050 ~8,133 0.1% 71 682 11.1%

Western ~13,000 ~12,000 -0.3% 110 550 9.0%

Europe

East Asia ~3,100 ~7,800 5.1% 27 454 12.1%

Central/ ~1,000 ~3,300 5.0% 8 280 13.5%

Eastern Europe

Latin America ~700 ~750 0.3% 6 45 8.0%

Africa ~450 ~680 1.6% 4 40 9.0%

MENA ~850 ~1,450 2.4% 7 100 10.0%

South Asia ~320 ~980 4.5% 3 84 14.0%

Strategic Gold Shift

Central banks in Russia, China, and emerging markets like Uzbekistan, Kazakhstan, and India drove a gold buying

renaissance from 2000-2024, amassing over 4,449 tonnes collectively-far outstripping sales by Western holders

like Switzerland and France, which lost over 2,000 tonnes net. This deliberate accumulation signals a strategic

pivot from U.S. dollar reliance toward gold as a hedge against geopolitical risks and currency volatility.

Recent years (2020-2024) intensified this trend, with China, Turkey, Poland, and India adding over 1,000 tonnes

amid global uncertainty, underscoring gold's resurgence as a core reserve asset despite sellers like Kazakhstan.

The pattern reveals a multipolar rebalancing, where Eastern banks architect monetary resilience.

Changing Reserve Composition: Gold Reclaims Its Place

The most telling development lies not just in tonnes, but in gold’s rising share of total reserves. A renewed

appreciation of gold as a non correlated, universally accepted asset reshaped portfolio construction across many

central banks. Countries such as Uzbekistan, Turkey, Russia, Kazakhstan, China, and India materially lifted gold’s

share of reserves, with mid sized economies like Egypt, Qatar, and Poland joining the trend. Meanwhile, long

time holders - Switzerland, the UK, France, the Netherlands, Spain - saw gold’s weight decline after early 2000s

sales under formal gold sale agreements. “Gold’s comeback in reserve portfolios reflects more than value; it

symbolizes independence in a multipolar world.”

India’s Quiet but Decisive Shift

India’s journey over the past quarter century encapsulates this broader transformation. In 2000, gold was a small,

almost residual entry on the Reserve Bank of India’s balance sheet, at about 395 tonnes and roughly 2% of total

reserves. By 2024, holdings had more than doubled in volume and multiplied in value, pushing gold’s share close

to 5.5% and signalling a clear strategic re rating of the asset.

39