Page 38 - Bullion World Issue 01 Volume 06 January_2026

P. 38

Bullion World | Volume 6 | Issue 01 | January 2026

TWO DECADES OF GOLD STRATEGY: HOW CENTRAL

BANKS REDEFINED THEIR RESERVES (2000–2024)

Mr Prathik Tambre, Senior Analyst - Precious Metals, Bullion World

Introduction

At the dawn of the millennium, gold looked like yesterday’s asset. Western central banks were net sellers, global

finance revolved around the dollar, and bullion appeared destined to remain a residual line on official balance

sheets. By 2024, the script had been dramatically rewritten. Central banks - especially in emerging markets -

had orchestrated a quiet but profound comeback for gold, turning from sellers into some of the market’s most

consistent buyers. “From forgotten relic to strategic reserve - gold’s comeback has reshaped how nations think

about monetary security.”

The Big Picture: From Stability to Surge

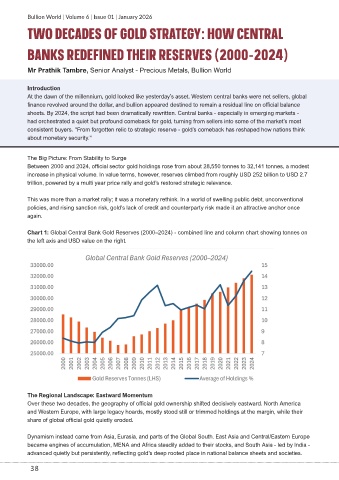

Between 2000 and 2024, official sector gold holdings rose from about 28,550 tonnes to 32,141 tonnes, a modest

increase in physical volume. In value terms, however, reserves climbed from roughly USD 252 billion to USD 2.7

trillion, powered by a multi year price rally and gold’s restored strategic relevance.

This was more than a market rally; it was a monetary rethink. In a world of swelling public debt, unconventional

policies, and rising sanction risk, gold’s lack of credit and counterparty risk made it an attractive anchor once

again.

Chart 1: Global Central Bank Gold Reserves (2000–2024) - combined line and column chart showing tonnes on

the left axis and USD value on the right.

The Regional Landscape: Eastward Momentum

Over these two decades, the geography of official gold ownership shifted decisively eastward. North America

and Western Europe, with large legacy hoards, mostly stood still or trimmed holdings at the margin, while their

share of global official gold quietly eroded.

Dynamism instead came from Asia, Eurasia, and parts of the Global South. East Asia and Central/Eastern Europe

became engines of accumulation, MENA and Africa steadily added to their stocks, and South Asia - led by India -

advanced quietly but persistently, reflecting gold’s deep rooted place in national balance sheets and societies.

38