Page 10 - Bullion World Issue 02 Volume 06 February_2026

P. 10

Bullion World | Volume 6 | Issue 02 | February 2026

KEY HIGHLIGHTS:

UNION BUDGET 2026

CA Bhargava Vaidya & CA Bhakti Vaidya

Income-tax Act, 2025 (replacing the Income-tax Act, 1961) will be in force

from 1 April 2026. The Hon’ble Finance Minister announced that the

simplified Income tax rules and forms will be notified shortly.

Some of the key announcements of the Budget 2026 are discussed below

INCOME TAX PROVISIONS

Tax rates kept constant

• No changes have been proposed in the tax rates for individuals, Hindu Undivided Families (‘HUFs’),

firms or companies.

• In order to encourage companies in the old regime to move to the new tax regime, it is proposed that MAT

paid under the old regime will be treated as final tax and no new MAT credit will be allowed. The MAT rate is

proposed to be reduced from 15% to 14% of book profit and MAT credit set-off will be allowed only under the

new regime, limited to 25% of tax liability.

CHANGES IN RELATION TO FILING OF INCOME TAX RETURNS

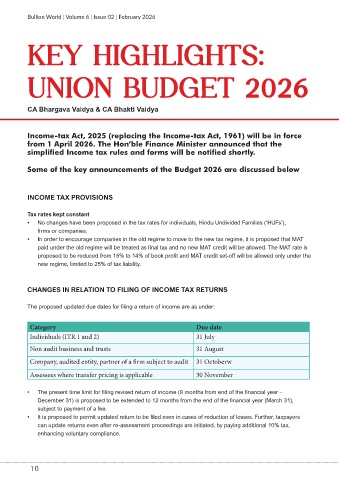

The proposed updated due dates for filing a return of income are as under:

Category Due date

Individuals (ITR 1 and 2) 31 July

Non audit business and trusts 31 August

Company, audited entity, partner of a firm subject to audit 31 Octoberw

Assessees where transfer pricing is applicable 30 November

• The present time limit for filing revised return of income (9 months from end of the financial year –

December 31) is proposed to be extended to 12 months from the end of the financial year (March 31),

subject to payment of a fee.

• It is proposed to permit updated return to be filed even in cases of reduction of losses. Further, taxpayers

can update returns even after re-assessment proceedings are initiated, by paying additional 10% tax,

enhancing voluntary compliance.

10