Central banks bolster gold reserves further in February, albeit at a slower pace

Wed April 03 2024

- Central banks bought a net 19 tonnes (t), down 58% m/m1

- Demand continues to be driven by emerging market banks, such as China and India

- The slower pace of accumulation in February has had little impact on the broad trend in central bank buying

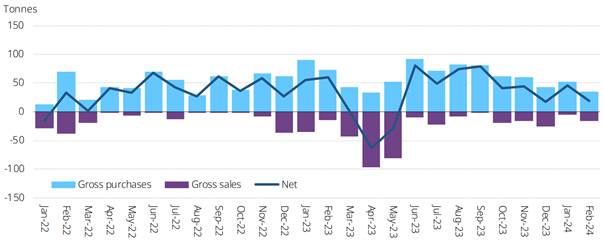

Available data for February shows that reported global central bank gold reserves rose by 19t, the ninth consecutive month of growth. But a combination of slower gross purchases and a higher volume of sales meant that February’s buying was 58% lower than January’s total of 45t. On a y-t-d basis central banks report the addition of 64t over January and February, 43% lower than the same period in 2023 but a fourfold increase on 2022.

Central bank gold demand slowed in February

Monthly central bank gold purchases and sales*

*Data to February 2024 where available.

Source: IMF IFS, respective central banks, World Gold Council

As in preceding months, activity was mostly limited to those who have been regular buyers/sellers in recent years.

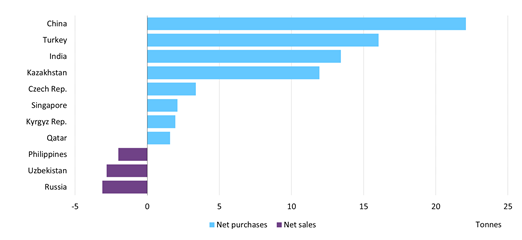

- The People’s Bank of China was the largest buyer in the month, increasing its gold reserves by 12t to 2,257t. Including February, PBoC’s gold reserves have grown for 16 consecutive months, although gold’s share of total reserves remains around 4%

- The National Bank of Kazakhstan increased its gold reserves by 6t in February, continuing its strong start to 2024. Y-t-d net purchases now amount to 12t, lifting total holdings to just over 306t

- Weekly data from the Reserve Bank of India showed its gold reserves rose by a further 6t in February. This lifts its y-t-d buying to over 13t and total gold holdings to 817t

- Official gold reserves at the Central Bank of Turkey rose by 4t in February, lifting holdings to 556t2

- The Monetary Authority of Singapore added 2t to its gold reserves during the month, first increase in gold holdings since September 2023. Gold reserves now total 232t

- Czech National Bank data shows its gold reserves rose by around 2t in February – the twelfth straight month of gold buying (of 1t or more). Over that period Czech buying has totalled almost 22t, lifting gold holdings to 34t, 183% higher than at the end of February 2023

- The Qatar Central Bank reported that its gold reserves rose by nearly 2t in February. Its total gold holdings surpassed 100t in December, and now stand at just below 103t

- Data from the National Bank of the Kyrgyz Republic showed that its gold reserves rose by more than 1t in February, with y-t-d net purchases now totalling 2t. Total gold holdings now stand at almost 24t

- Available data shows that there were only two notable sellers during the month. The Central Bank of Uzbekistan reduced its gold reserves by 12t during the month, while the Central Bank of Jordan lowered its gold holding by 4t.

Central bank purchases comfortably outweigh sales y-t-d

Individual central bank net purchases/sales in tonnes*

*Data to February 2024 where available.

Source: IMF IFS, respective central banks, World Gold Council

Despite slower demand from central banks in February, the year has got off to a healthy start and the broad trend of gold buying remains intact. Look out for our next Gold Demand Trends report in late April, which will cover central bank demand for the entire first quarter.

Footnotes

- Based on monthly IMF IFS data (reported with a two-month lag) and supplemented with data from respective central banks where applicable. Most institutions report on a regular basis, but some may report with a – sometimes significant – delay. Late availability of data may lead to revisions. The data reported here informs, but is distinct from, the central bank demand estimates we report in Gold Demand Trends.

- Turkey’s official sector gold reserves are the sum of central bank-owned gold and Treasury gold holdings. This is equivalent to gross gold reserves less all gold held at the central bank in relation to commercial sector gold policies (such as the Reserve Option Mechanism (ROM), collateral, deposits and swaps)

Source: https://www.gold.org/